Have you ever seen something advertised so much that you just can’t escape it?

You’re watching a YouTube video about marketing, and an ad pops up. You’re scrolling through Facebook, and there it is again. A slick, exciting ad promising a “secret” path to wealth. They’re talking about a financial product called an Indexed Universal Life (IUL) insurance policy.

The ads are everywhere. They feature smiling families and confident entrepreneurs. They make huge promises: “Market gains without the risk!” “Tax-free retirement income!” “A safety net that also makes you rich!”

It sounds almost too good to be true, doesn’t it?

Well, I’m here to ask you a critical question that every smart entrepreneur should consider:

If this IUL product is such a revolutionary, no-brainer wealth-building machine, why does it need a multi-million dollar, non-stop advertising blitz to convince people to buy it?

Think about the best, most reliable tools you use in your business. The ones that truly work and make you money aren’t sold with flashy hype and vague promises. They are sold on their proven, straightforward results. The need for constant, exciting advertising is often the first red flag. It usually means the product itself is complicated, expensive, and hard to sell on its actual merits.

Lately, my feed has been flooded with these IUL ads, and it set off all my alarm bells. In the world of online marketing, we know that if an offer requires overwhelming hype, there’s almost always a very steep downside hiding in the fine print.

And I’m not the only one who’s noticed. The shocking truth about IULs is now exploding into public view, with one of America’s most famous athletes leading the charge. His story is a powerful warning for every business owner and affiliate marketer looking to protect and grow their hard-earned money.

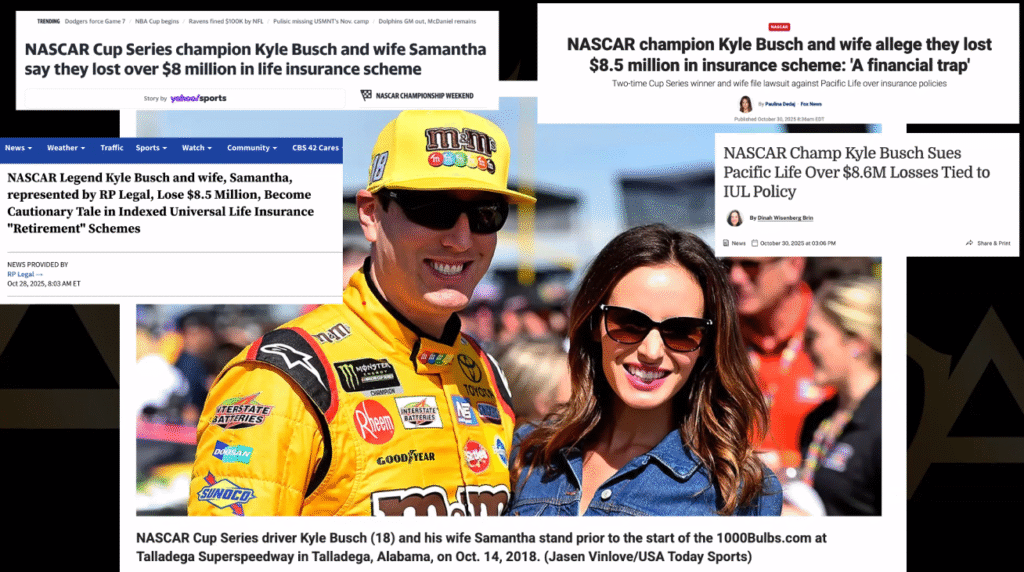

The $8.6 Million Warning Shot: Kyle Busch’s IUL Disaster

You know Kyle Busch. He’s a NASCAR champion, a fierce competitor who understands speed, risk, and precision. He’s a savvy businessman who built an empire from his talent. He’s not someone you’d expect to fall for a bad financial deal.

But in October 2025, Kyle Busch made headlines not for his racing, but for his lawsuit. He sued Pacific Life, a major insurance company, over an IUL policy that he claims cost him a staggering $8.6 million.

Let that number sink in. $8.6 million. That’s life-changing money for anyone, even for a champion athlete.

What happened? According to the lawsuit, Busch was sold an IUL policy as a powerful investment vehicle. He was likely told the same story you see in the ads: the potential for market-linked gains with a protective floor against losses. He paid massive premiums into the policy, expecting it to build significant cash value for his future.

But the policy didn’t perform as advertised. Instead of growing steadily, the complex mechanics of the IUL—the caps, the fees, the participation rates—eroded its value. The lawsuit alleges that Pacific Life failed to properly manage the policy's “economic fundamentals,” leading to catastrophic losses.

Kyle Busch, a expert in managing high-stakes risk on the track, had his financial future derailed by the hidden risks of a product marketed as “safe.”

This isn’t just a story about a wealthy celebrity. This is a cautionary tale for anyone with an income to protect. If a team of financial advisors for a NASCAR champion can get it so wrong, what chance does the average entrepreneur or affiliate marketer have against the fine print?

A System-Wide Problem: Why Almost Every IUL Provider Is Being Sued

Now, here is the most damning part of all. Kyle Busch’s lawsuit is not an isolated event. It is part of a tidal wave of litigation.

Pacific Life, the company Busch is suing, is also facing a massive, nationwide class-action lawsuit. But they are far from alone. Almost every major insurance company that sells IULs is facing similar legal battles.

- Nationwide Life is being sued by policyholders.

- Minnesota Life is facing a class-action suit.

- Security Benefit Life and Lincoln National Life are also defending themselves against similar allegations.

The lawsuits all tell a familiar story. Policyholders claim they were misled. They allege the insurance companies hid the true impact of fees and how difficult it would be for the policies to accumulate cash value. They argue that the “illustrations” (the fancy sales charts showing future growth) were based on unrealistic, optimistic assumptions that would never come true in the real world.

When you see a pattern this widespread, it’s no longer about a few “bad apple” salesmen. It points to a fundamental flaw in the product itself. The entire business model of IULs seems to be under legal assault because the reality for consumers has been so different from the sales pitch.

This is a coordinated, legal reckoning for an entire industry. And it’s happening right now.

Demystifying the IUL: How a “Safe” Investment Bleeds You Dry

So, what exactly makes IULs so problematic? The devil is in the details—the complicated details that salespeople gloss over. Let's break down the four main mechanisms that drain your money.

1. The Illusion of “Uncapped” Growth: The Secret Cap

This is the most seductive part of the sales pitch. “When the market goes up, you make money! When it goes down, you don’t lose anything! It’s a win-win!”

This is a half-truth. While it’s often true that your account has a “floor” (usually 0%) that protects you from losses, there is almost always a ceiling or a cap on your gains.

Here’s how it works in practice:

- Let’s say the S&P 500 has a fantastic year and gains 18%.

- Your IUL policy might have a “cap rate” of 10%.

- This means that even though the market grew by 18%, your account is only credited with a 10% gain.

- The insurance company pockets the difference.

You are trading away your potential for full market growth in exchange for that downside protection. Over 20 or 30 years, missing out on those extra years of strong growth can cost you hundreds of thousands, or even millions, of dollars in compounded returns. This is likely a core part of what went wrong in Kyle Busch’s policy.

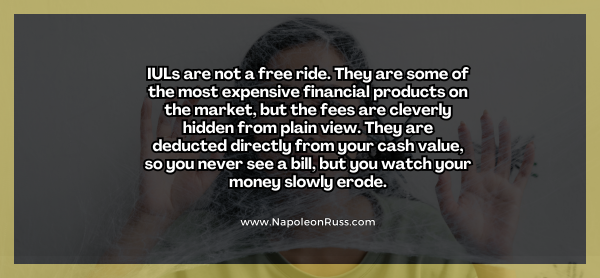

2. The Silent Killer: The Mountain of Hidden Fees

IULs are not a free ride. They are some of the most expensive financial products on the market, but the fees are cleverly hidden from plain view. They are deducted directly from your cash value, so you never see a bill, but you watch your money slowly erode.

These fees include:

- Cost of Insurance (COI): The actual price of the death benefit. This isn't fixed; it increases every year as you get older.

- Administrative Fees: Monthly or annual charges for “managing” the policy.

- Mortality and Expense Risk (M&E) Charge: A fee to cover the insurer’s risk and profit.

- Rider Fees: Costs for any add-ons, like disability waivers.

Unlike a simple index fund that might charge a 0.05% fee, the total cost of an IUL is complex and often opaque. It can easily add up to 2-4% or more per year, creating a massive drag on your cash value's ability to grow.

3. The Moving Goalposts: Participation Rates and Spreads

If the cap wasn’t enough, insurance companies have other levers to pull. Many policies use a “participation rate” or an “asset fee spread.”

- Participation Rate: This determines how much of the index's gain you get. A 100% rate means you get the full gain (up to the cap). But if the company lowers it to 70%, and the index goes up 10%, you only get 7%.

- Spread Fee (or Asset Fee): This is a direct deduction from your gains. For example, if the index gains 10% and the spread is 3%, your account only gets credited 7%.

The critical thing to understand is that these rates are not guaranteed. The insurance company can adjust the cap, the participation rate, and the spread every single year. The “rules of the game” can change after you’ve already poured your money in, leaving you with dwindling returns.

4. The Dangerous “Tax-Free Loan” Strategy

Salespeople love to pitch the “tax-free loans” you can take from your cash value. They frame it as accessing “your own money” tax-free.

This is dangerously misleading. These are policy loans from the insurer, not withdrawals of your own cash. They charge you interest to borrow your own money.

The catastrophic risk, as highlighted in many lawsuits, is that if the policy ever lapses or is surrendered with an outstanding loan, the IRS considers that loan to be a distribution. This can trigger a massive, unexpected income tax bill on the entire loan amount. People have lost their policies and been hit with six-figure tax bills because of this misunderstood feature.

The Better Way: “Buy Term and Invest the Difference”

As entrepreneurs, we understand the power of simple, effective systems. We don’t need complicated, multi-tools that perform multiple tasks poorly. We need the best tool for each specific job.

When it comes to your financial security, the same logic applies. The IUL tries to be both an insurance product and an investment product, and it fails at both.

The time-tested, proven alternative is the “Buy Term and Invest the Difference” strategy.

Here’s how it works:

Step 1: Buy Pure, Cheap Insurance. Purchase a level-term life insurance policy for 20 or 30 years. This is pure death benefit protection. It’s simple, straightforward, and incredibly affordable. It does one job perfectly: ensuring your family’s financial security if the unthinkable happens. This is your safety net.

Step 2: Invest the Rest Like a Pro. Take the significant amount of money you save by not buying an expensive IUL and systematically invest it in a tax-advantaged retirement account like a Roth IRA or a Solo 401(k). Inside that account, you can invest in low-cost, broad-market index funds or ETFs.

Why this is a vastly superior strategy:

- True, Uncapped Growth: You get 100% of the market's returns, not a capped version.

- Radical Transparency: You see the fees (they are tiny), and you control your investments.

- Proven Results: The long-term data overwhelmingly shows that this simple, disciplined approach builds more wealth than complex, high-fee insurance products.

- Liquidity and Control: Your investments are not locked up with surrender charges. It’s your money, in your account.

Your Financial Future Deserves Better Than Hype

The story of Kyle Busch and the wave of lawsuits against IUL providers is not a coincidence. It is the inevitable result of a product whose complexity obscures its poor performance and high costs.

You have worked too hard to build your online income through affiliate marketing, network marketing, and sales to see it eroded by a hyped-up product with a history of devastating its owners.

You don’t need flashy ads and empty promises. You need clarity, transparency, and a strategy that actually works.

Your financial plan should be as straightforward and effective as your best sales funnel. It should be built on a foundation of proven principles, not on the shifting sands of caps, participation rates, and hidden fees.

Don’t let the hype drown out the truth. Choose the simple, proven path to building and protecting the wealth you are working so hard to create.

💫 You were never given a dream without also being given the power to make it come true.

— Napoleon Russ

")